The Long Tail of the Cost of Living Crisis

What we're feeling around the houses

We were posed a question from a client last week that got us thinking, and gave us an excuse to put together and share some thoughts.

The client asked us:

“Someone in the Board Meeting I was just in said ‘the cost of living crisis is over’ - do you have any thoughts based on our project and beyond?”

Obviously they were asking for a response based on our interactions and learnings from the people we go and meet all over the country, not because we’re economic experts. (Because we’re not!)

And - before the keyboard warriors come out - we’re in no way saying our thinking below is quantifiable or scientifically robust.

As we always say, our output:

Uncovers interesting insights, it is not irrefutable evidence.

But her question prompted us to try and make sense of many things we’ve been seeing and feeling on our travels, combined with some reports we’ve been reading too.

And please bear in mind over the past year or so we’ve met with a huge range of people: single mums in social housing, aspiring professional comedians, HNWIs with swimming pools out back, organic farmers, students, people passionate about sustainability and everything in-between.

SOME THOUGHTS

The word ‘over’ in the question above is something that acted like a magnet to our thinking. It was the first thing we focused on. It’s a very definitive word.

Across all the visits and observations we conduct for a plethora of clients (and for personal passion projects), we’ve seen nothing in any of the visits that makes us think it’s ‘over’ - as in ‘life is back to normal.’

And that’s for a fairly obvious reason: The world - and the economy - is now a different place to what it was before ‘the cost of living crisis’ started.

Our hypothesis is:

“We’re into the Long Tail Phase of the Cost of Living Crisis”

THE LONG TAIL OF THE COST OF LIVING CRISIS

People are telling us they feel like we’re through the big painful hump, the ‘Truss era’ that seems like a bad dream to many, but the overall ‘cost of living crisis’ is not feeling ‘over’ to people.

What we’re seeing is how that ‘short sharp shock’ in October 2022 is impacting everyday life now and the expectation from them that it’ll also impact their immediate futures.

There are three areas we’re seeing and feeling. One is something we’re seeing more and more now, the other two are things we’re starting to see and feel more, and are interested if we see more of over the coming year or two.

1 - LIVING WITH THRIFTY BEHAVIOURS

Everyone - everyone - we have met over the past year or so is exhibiting some kind of behaviour around the concept of thriftiness.

Yes, thriftiness means different things to different people, and creates different behaviours in different people. For some it’s about earning just that little bit more ‘off the books’ and for others it’s about buying and re-selling second hand goods more than they have in the past.

It’s thriftiness through an entire cycle - from earning a little bit more how they can, to spending a little less where they can, to selling latent value they have around their home, to selling specific items bought to be re-sold, and accruing credit via apps like Vinted that make them feel like they have ‘earned’ a treat.

We’ve met people working down the local market on a Saturday morning for an extra £80 cash-in-hand every month - so they can pay for their holiday in cash (so it’s not tracked and doesn’t put their benefits at risk).

We’ve met people accruing sneaker collections as mini-investments. Latent money they can ‘cash in’ when they need it.

Kyle brought this to life well. Having is own ‘Vinted Corner’ that we’re seeing more and more. And you can see more on the post over here.

Even HNWIs we’ve met shared some of their thrifty behaviours. From searching online for voucher codes, to teaching their daughter the value of money via Vinted. All the while having a bunch of Rolex’s on the bedside table.

Hypothesising around the impact of growing thriftiness is interesting. Below is a model we have used in previous projects.

There’s an interesting provocation here about whether this 15 year-old model needs to be evolved.

This was designed pre-delivery economy, pre-Amazon prime, pre-TEMU, and pre-Vinted. It was before behaviours around the delivery economy (and the returns economy) were artificially accelerated due to the pandemic.

There’s an interesting exercise to interrogate the above to include the beliefs and behaviours around thriftiness and reselling. Certain items and categories people are now buying more of, or buying and having a different relationship with - i.e. having one eye on reselling it when they buy it.

What does this mean for brands? As easy returns become more important? As products holding their prices becomes more important? What does this mean for price elasticity? What does it mean for people’s purchasing decisions? Do they look less at the brand, and more at logistical concerns such as where their closest Evri locker is?

Our visits are indicating to us this thriftiness behaviour is not about people being happy to lease or rent products. The ‘sugar rush’ of buying things they own is still ingrained in lots of people, but them having a ‘get out clause’ of an option to re-sell the item is appealing. We’re seeing the ‘sugar rush’ of buying new things being augmented by a ‘sugar rush’ of accruing value in-apps, that can be transferred into ‘treats’.

Selling lots of things you don’t need, transforms into an opportunity to get something you want.

The role of the home, and sections of the home are evolving too - with the homes we’re visiting regularly having packages hanging around that are coming or going, or goods hung up on the outside of a wardrobe because they’ve just been photographed and listed on an app.

The fact the Government have changed the tax regulations around second-hand selling tells us it’s happening at scale and is likely to be around for a while. They wouldn’t change the law unless they feel they’re missing out on something.

2 - FISCAL DRAG

This is something we’ve all heard in the news but something we’re starting to feel, and are interested to see if we’ll see more of over the coming year or two.

Essentially, interest rates may have made some salaries go up, but the tax bands haven’t really changed, and what people are spending on daily life has gone up.

Which means over the coming tax year or two, even if you are earning a little more, you’re likely paying more tax and will actually have less disposable income to spend.

There’s a sense of helplessness, and a loss of control we’re picking up on:.

'“I think I’m going to be better off with my salary increase, but I’m not sure yet. As other bills have gone up, and I’ll lose some benefits, and pay more tax, I don’t really know yet. I have to wait and see…”

(That’s not a direct quote from a participant - but an amalgamation from several).

And no doubt if there’s a new government in charge after the next election, they’ll get the blame (as people tend to have short memories and want instant improvements), but the die is already cast.

From Martin Lewis’s Money Saving Expert Newsletter recently:

'NI and income tax thresholds have been frozen since 2021 (slight changes in Scot) while earnings and especially prices have risen. The result... more of people's income goes to tax. This way of increasing tax revenue is called 'fiscal drag'.

It's estimated that even after NI cuts, workers who earn under £26,000 and over £60,000 will be worse off in 2024/25. Those in between will be better off (especially those nearing £50k); those who don't work (eg, pensioners and those with unearned income) will mainly pay more tax. (Source: Institute for Fiscal Studies.)’

That’s a big chunk of your audience having less money to buy your products.

That’s a big chunk of your audience trading down.

That’s a big chunk of your audience being thriftier.

That’s a big chunk of your audience feeling even less in control.

And the kicker for lots of the participants we meet is that those negative impacts aren’t a result of anything they’ve done - those impacts have been totally beyond their control.

What does that do for their mindset? For their sense of belief in the political system? What does it mean for the perception of ‘necessities’ versus ‘luxuries’?

We’re seeing what this means for specific categories.

A recent FMCG project had us screening people with a range of questions.

Examples - to maintain anonymity:

“Do you earn between £x - £y?”

”Who is your energy provider?”

”Do you have [premium branded item] in your fridge right now?”

The last question was the real one we wanted to know the answer to - the questions before it (and others) being dummy questions so the participants didn’t know why we were visiting.

They all said they did have the [premium branded item] in the fridge, yet when we visited only a certain proportion did.

The others had the ALDI/ LIDL equivalent item in their fridge. They had unconsciously traded down. In focus groups that reality wouldn’t have been picked up, but what it means for [premium branded item] is they need to figure out how to build a bridge that spans the ‘price delta’ to justify someone buying their product and not a lookalike.

From FMCG, to holidays: We’re seeing how important holidays are to people, with the vast majority - by hook or by crook - getting away if they can. They can’t control how bad it’s getting at home, but they’ll do everything they can to escape it to their happy place (physically and mentally) - if only for a week or two.

The impact this is having on family dynamics is noticeable, with typically one of the relationship being the ‘instigator and persuader’ that needs to pull the other along on the purchasing journey. Then going on holiday and being on emotional tenterhooks as to whether they get the ‘nod of approval’ that they did well or not from their partner and/or children. A high consideration purchase for sure, but highly emotional too.

3 - SHORT-TERM ACTIONS IMPACTING THE NOW AND FUTURE

Last year we met a bunch of people who were “just getting through today”. (Again, an amalgam of several people).

A direct quote from someone we chatted to about a project around community and family:

"If more people adhered to ‘look after your family instead of the world’ I think we’d all be a bit better off”

That epitomises a sense of last year from people:

“I want to be a good citizen, I want to do more [for sustainability], but I need to look after me and my own to get through these tough times”

(An amalgam).

And to get through, some people have had to make short-term choices. They’re looking 5 days ahead not 5 years or 5 months ahead.

People have had to make big decisions just to survive.

And ‘surviving’ doesn’t just mean people having to use a Food Bank.

It means choosing which bills to pay month on month, and rotating where you pay your bills so you don’t get cut off, you just accrue more debt and delay payments. It’s no surprise mortgage arrears are up 50% year on year.

And it’s not just mortgages - it’s the whole gamut of household services.

Now - the reality here is the mortgage and energy companies will get that money back somehow. They’re not in the business of letting debts pass them by.

So the people who have had to make choices to delay or default, who are in arrears (through no fault of their own), aren’t going to be flush for a while.

If you combine fiscal drag with debt repayments, in a stagnant economy then they aren’t moving forward at all.

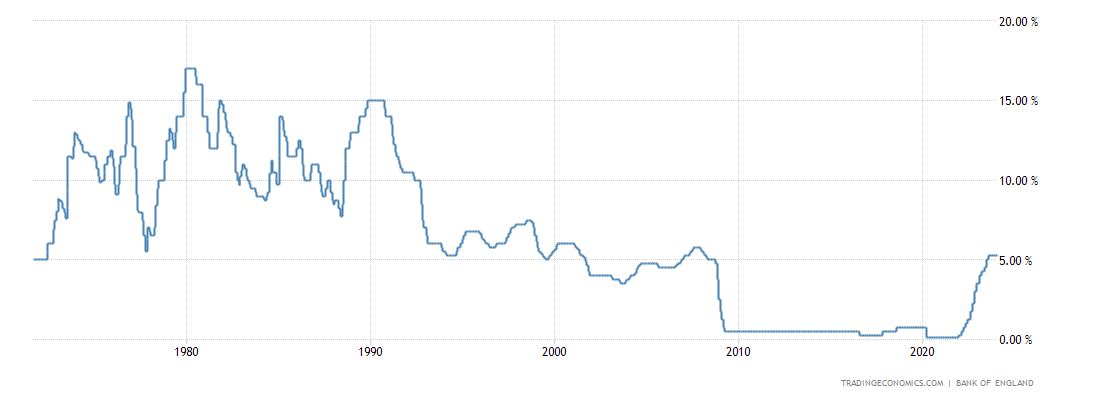

We’re also told up to 1.5m people’s fixed rate mortgages expire this year.

The current base rate is at 5.25% (at the time of writing), and if we presume that those 1.5m fixed rate mortgages expiring are coming out of 2-year and 5-year fixed deals, that means their new rate is likely to be anywhere between 3x to 5x the interest rate they had previously. Look at where the blue line is now (5.25%) and where it was 2 and 5 years ago (hovering around the 1% mark)… (That’s base rate, not mortgage rates - but we know they track obviously).

In reality - that little lift of a blue line on a chart is HUNDREDS of pounds difference month on month for millions of households - thousands of pounds even. (Obviously there are lots of variables).

The UK average salary is £34,900, which works out at roughly £2,300 a month NET. If you take an extra few hundred quid out of that you’re gonna feel it…

And it’s just money lost in a void. It’s the payment of more money for exactly the same thing - but costing you lots more.

You’re not getting a better product or a better experience. You’re not getting the ‘sugar rush’ of buying something exciting. You’re not experiencing anything new.

It’s another example of a lack of control in the lives of people around the country. A perception that other people created the problem, and other people are benefitting whilst they suffer.

Saanvi when we met her said of her upcoming remortgage:

"It's about 500 pounds extra we'll have to pay [per month]. That's a lot of money. So after the mortgage, of course, after it's renewed, then we'll have to check what we can do.”

Saanvi is middle class, living in Ascot with her husband and two kids. An extra £500 a month, lost in a void, will have a huge impact on her life. And not just hers, but her children’s too.

That change will directly impact her behaviours around sustainability. When we met her she was part way through investigating whether to buy a [high consideration sustainable energy product] but with her and her husband having to dip into their savings to get by, and with the cost of the new item being added to the (new, more expensive) mortgage not being an option, it was becoming less likely she would go through and complete the purchase.

And that’s just for those lucky enough to be on the property ladder… for the younger generation it’s no better, with a recent report stating 29% of 18- to 24-year-olds had missed three or more credit or bill payments in the last six months.

Would any of the above say the ‘cost of living crisis’ was over?

SOME CLOSING THOUGHTS

We are not economic experts. And we’re sure we could find research either way to prove that the cost of living crisis IS over, or IS NOT over.

We simply visit lots of people in different situations, around the UK, listen to them and observe what we see. And we wanted to share some of our thinking with you.

We’re very cognisant too that we won’t be going into any future conversations with participants with the above in mind. There’ll be no confirmation bias happening here. We’ll go in as we always do: Brand blind participants, no leading language from us (we never use the language ‘cost of living crisis’ until the participant brings it up), and with a reality first brand second approach.

Put simply, we try and find out what’s important to them, and the above areas have been ringing out loud and clear.

If you’re a brand, there’s a lot in the above. A lot of things that need to be thought about:

The impact of thriftiness in your category and brand. What does it mean for your Reasons To Believe?

The impact of the non-negotiables (like holidays) and on premium branded goods (if people are prepared to swap for lookalikes).

Whether your ‘sugar rush’ experience of purchasing is delivering something similar to the ‘earned' sugar rush’ of apps like Vinted?

If Fiscal Drag and Deferred Payments will affect your target audience’s spending over the next year or so. Is your biggest competitor another brand in your category, or mortgage renewals and debt repayments?

We’ll keep travelling around, seeing, hearing, and feeling. And we’ll keep on sharing some thoughts with you…

… but if you have specific questions about how the above may relate to your brand and category now and in the future, you know where to come…

This is great Mark - I think it's easy for people who have been isolated from the worst of it to feel like when it comes to the cost of living because it's a crisis that's been going on a while, it's over.

That mortgage point is so important, as there's such a big lag between interest rates going up and people feeling the impact of that.

In the meantime, inflation has come down...but prices are still going up, and have gone up 20-30% for some essentials over the last two and a bit years.

So, with inflation down, but the hit of mortgage rates going up only now being felt, it's going to feel odd to people - the pain continues, even as the headline number falls.